The Death of the "Inpatient Only" List: Who Captures the 2026 Margin?

- Anshul Jain

- 1 day ago

- 3 min read

The structural migration of orthopedic and spine surgery from traditional inpatient towers to outpatient settings is no longer a passive market trend; it is a federal mandate. Driven by the continuous dissolution of the Centers for Medicare & Medicaid Services (CMS) Inpatient Only (IPO) list, high-acuity spinal fusions, total joint arthroplasties, and complex reconstructions are officially clearing for the Ambulatory Surgery Center (ASC) setting.

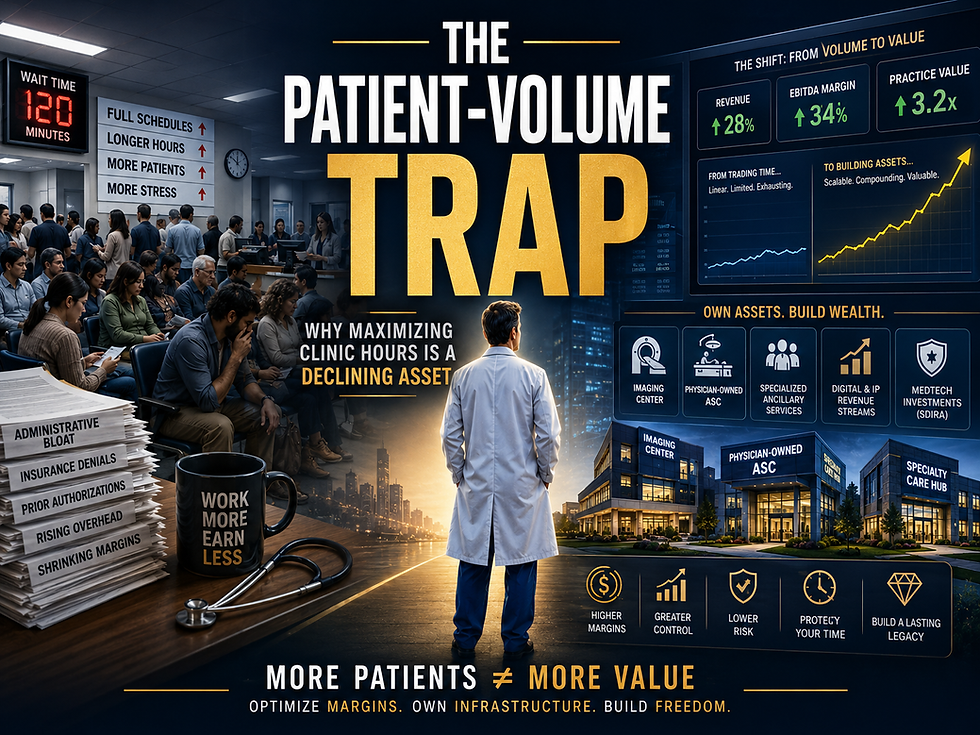

For the private physician investor, this regulatory shift represents the largest wealth transfer in modern U.S. surgical history. The critical question for 2026 is not whether your cases will leave the hospital, but who will own the specialized infrastructure that receives them.

The Mechanics of the Outpatient Migration

1. The Asymmetry of the Professional Fee

When a complex spine or orthopedic case moves from an inpatient OR to an outpatient facility, the surgeon’s personal reimbursement remains fundamentally flat.

The Clinical Context: You face the exact same clinical risks, utilize the same technical precision, and dedicate the same intraoperative time whether a multi-level decompression is performed in a legacy hospital or an independent ASC.

The Financial Reality: Under the Medicare Physician Fee Schedule, your professional fee does not scale with site efficiency. If you do not hold equity in the site of service, you are absorbing the operational stress of higher-acuity outpatient cases while giving the real profit engine—the facility fee—away to an institutional landlord.

2. ASC Reimbursement Parity

Recent CMS updates have narrowed the historic payment gap between Hospital Outpatient Departments (HOPDs) and independent ASCs, applying consistent inflation updates to stabilize outpatient facility margins.

The Macro Shift: This pricing alignment means that specialized, lean ASCs can now capture institutional-grade facility revenue without the bloated, non-clinical overhead costs that cripple traditional hospital balance sheets.

The Enterprise Value: By shifting appropriate surgical volume into an ASC where you hold equity, you turn an everyday clinical decision into a high-yielding corporate distribution, structurally multiplying the terminal value of your practice.

3. The Corporate Race for Block Time

Recognizing this outpatient cash surge, corporate health systems and national management chains are racing to buy up local ASC real estate, attempting to convert independent surgeons into high-volume tenants.

The Structural Defense: Protecting your practice requires moving from a volume-producer mentality to an Infrastructure Owner model. Syndicating with regional peers to anchor early-stage equity in local clinical platforms ensures you dictate your own block times, choice of technology, and clinical pathways.

The Bottom Line: Owning the Site of Service

Uncertainty only breeds fear when you operate as a passenger inside someone else's infrastructure. The elimination of the IPO list is an unprecedented regulatory greenlight for independent surgical platforms.

Stop gifting your high-acuity volume to institutional systems that treat your clinical expertise as a depreciating asset. Reclaim your financial sovereignty, integrate your delivery model, and build your legacy on ground you own.

Analyzing the Financial Migration

To evaluate the exact shift in capital distribution, we look at the financial performance of identical procedures across three distinct environments: Hospital Employment (W2/Inpatient), Hospital Outpatient (HOPD Non-Owner), and a Physician-Owned ASC.

While professional fees remain capped, the variance lies entirely in your ability to capture the facility fee net margin and compound it into institutional enterprise value (calculated at a standard 10x EBITDA multiple for ASC equity platforms). Use the interactive model below to simulate your practice volume and calculate your true margin capture.

Comments